As you approach your golden years, you might naturally start thinking about how to financially secure your loved ones after you’re gone. Over 50s life insurance is a specific type of policy designed to address this very concern. Unlike traditional life insurance, it offers guaranteed acceptance without medical exams and provides a fixed payout to your beneficiaries when you pass away. This can be a valuable tool to ensure your family has the means to cover funeral expenses, outstanding debts, or anything else they might need during a difficult time.

However, it’s important to understand that over 50s life insurance comes with its own set of considerations. Because there are no medical checks, the premiums tend to be higher than traditional policies. Additionally, the payout amount is fixed, so it won’t grow over time. Let’s delve deeper into how it works and whether it might be the right fit for you.

Get affordable life insurance quotes for over 50s. Find the right coverage plan to protect your loved ones’ financial future.

What is Over 50s Life Insurance?

Over 50s life insurance, also known as senior life insurance, is designed specifically for individuals aged 50 and above. These plans typically offer simplified underwriting processes compared to traditional life insurance, making it easier to qualify for coverage regardless of pre-existing health conditions.

Benefits of Over 50s Life Insurance

Financial Security for Loved Ones

Provides a guaranteed payout to your beneficiaries upon your death, helping them cover expenses such as funeral costs, outstanding debts, or mortgage payments.

Peace of Mind

Knowing your loved ones are financially protected can alleviate stress and allow you to focus on enjoying your later years.

Guaranteed Acceptance

Over 50s plans often bypass medical exams, making them accessible to those with health conditions who might struggle to qualify for traditional life insurance.

Affordable Premiums

These plans are designed to be budget-friendly, with premiums typically lower than traditional life insurance due to the smaller payout amount.

Understanding Over 50s Life Insurance Options

There are two primary types of life insurance catering to the over 50s”

Term Life Insurance

This is the most affordable option, offering coverage for a specific period (10, 20, or 30 years). If you pass away within the term, your beneficiaries receive a death benefit payout. However, if you outlive the term, the policy expires without any cash value return.

Whole Life Insurance

This policy offers lifelong coverage, accumulating a cash value component over time. Premiums are typically higher than term life, but the cash value can be accessed through loans or withdrawals while you’re alive. Upon your passing, your beneficiaries receive both the death benefit and any accumulated cash value.

Choosing the Right Policy

Selecting the right life insurance policy depends on your individual needs and circumstances. Here are some key factors to consider:

Coverage Amount: Determine the amount of financial support your loved ones will need after you’re gone. Consider factors like final expenses, outstanding debts, and potential inheritance goals.

Budget: Be realistic about your budget and choose a policy with premiums you can comfortably afford throughout the term.

Health: Your health condition will influence your eligibility and premium costs. Be honest about your health during the application process.

Policy Length: For term life, choose a term that coincides with your financial obligations or desired coverage period.

Policy Features: Some policies offer additional benefits like accelerated death benefits for terminal illness or waiver of premium riders in case of disability.

How to Get Started with Over 50s Life Insurance

Here’s a roadmap to navigate the process of obtaining:

Gather Information: Research different life insurance companies and policy options. This guide provides a solid foundation, but further exploration is recommended.

Compare Quotes: Don’t settle for the first offer. Obtain quotes from multiple insurers to compare rates and coverage details.

Consider Using an Insurance Agent: A licensed insurance agent can help you assess your needs, recommend suitable policies, and guide you through the application process.

Read the Fine Print: Before finalizing any policy, meticulously review the terms and conditions, including exclusions, limitations, and benefits payout details.

Additional Considerations for Over 50s

Guaranteed Insurability Riders: These riders allow you to purchase additional coverage at specific points in the future without undergoing another medical exam, even if your health deteriorates.

Waiver of Premium Riders: These riders waive your future premium payments if you become disabled and meet specific conditions.

Long-Term Care Benefits: Some life insurance policies offer long-term care benefits that can help cover assisted living costs or nursing home care.

FAQs

Is Over 50s Life Insurance Expensive?

Premiums for over 50s life insurance are generally lower than traditional life insurance due to your age and potentially higher mortality rate. However, costs can vary depending on your health, coverage amount, and chosen plan.

Do I Need Over 50s Life Insurance if I Have Existing Coverage?

Review your existing life insurance policy to see if it provides sufficient coverage for your current needs. If not, an over 50s plan can supplement your existing coverage.

What Happens if My Health Condition Changes After Getting Over 50s Life Insurance?

Most over 50s plans offer guaranteed death benefits, meaning your beneficiaries will receive the payout regardless of future health changes.

Conclusion

Over 50s life insurance is an invaluable tool for safeguarding your loved ones’ financial future. By understanding your options, carefully evaluating your needs, and comparing quotes, you can secure the perfect policy that provides peace of mind and lasting security.

In today’s competitive real estate landscape, partnering with a reliable and efficient wholesale mortgage lender is crucial for success. United Wholesale Mortgage (UWM) stands out as a leader in the industry, offering exceptional service, innovative technology, and a commitment to empowering real estate agents and loan officers. This comprehensive guide dives deep into UWM’s offerings, exploring its advantages and how it can propel your business to new heights.

UWM’s dominant position in the wholesale mortgage market makes it a significant player in the home-buying process for many Americans. By providing a variety of loan options and streamlining the mortgage process for brokers, UWM helps facilitate a smooth experience for both brokers and borrowers.

What is United Wholesale Mortgage?

United Wholesale Mortgage (UWM), formerly known as United Shore Financial Services, is the biggest wholesale mortgage lender in the United States. Founded in 1986, it’s headquartered in Pontiac, Michigan. Unlike traditional lenders who deal directly with borrowers, UWM works with independent mortgage brokers. These brokers then offer UWM’s loans to their clients.

What does UWM do?

UWM acts as a lender for independent mortgage brokers. Brokers use UWM’s underwriting expertise and loan programs to secure financing for their clients. UWM offers a variety of mortgage products, including:

Conventional loans

FHA loans

VA loans

USDA loans

Jumbo loans

UWM is known for its innovative technology and commitment to fast turnaround times, which helps brokers close loans quickly and efficiently.

Why Partner with United Wholesale Mortgage?

The benefits of partnering with UWM are extensive, offering a competitive edge for real estate agents and loan officers alike:

Unmatched Speed and Efficiency

UWM boasts one of the fastest turn times in the industry, ensuring a smooth and timely loan approval process for your clients. This translates to quicker closings and happier clients.

Extensive Loan Portfolio

UWM offers a diverse range of loan products, catering to a wide variety of client needs. From conventional loans and FHA loans to VA loans and USDA loans, UWM has the perfect option to meet any borrower’s situation.

Competitive Rates and Flexibility

UWM consistently delivers some of the most competitive rates in the market, giving your clients access to the best possible deals. Additionally, UWM offers flexible underwriting guidelines, allowing you to work with a broader range of borrowers.

Industry-Leading Technology

UWM’s innovative technology platform, EASE (Empowering Agile Selling Environment), streamlines every step of the loan process. From loan application to closing, EASE provides a user-friendly interface with real-time tracking and clear communication, keeping you and your clients informed at all times.

Exceptional Customer Service

UWM prioritizes exceptional customer service, offering dedicated support teams to assist you throughout the loan process. Whether you have questions about specific loan programs or need guidance with complex scenarios, UWM’s team is always available to lend a helping hand.

Who can UWM help?

UWM works with independent mortgage brokers who help borrowers secure financing for their homes. UWM does not directly originate loans to consumers.

Becoming a UWM Partner

UWM offers a straightforward onboarding process to get you started quickly. Here’s what to expect:

Eligibility Requirements: Review UWM’s licensing and experience requirements to ensure you qualify for the partnership program.

Online Application: Submit a quick and easy online application to initiate the process.

Background Check: UWM conducts a thorough background check to ensure a secure and reliable partnership.

Compliance Training: Complete UWM’s comprehensive compliance training to ensure you’re up-to-date on industry regulations.

Welcome to the UWM Family: Once approved, you gain full access to UWM’s resources, support, and technology platform.

Unlocking the Full Potential of Your UWM Partnership

UWM goes beyond simply providing access to competitive rates and loan products. Here’s how to maximize your partnership:

Leverage UWM’s Educational Resources: UWM offers a wealth of educational resources, including webinars, workshops, and online courses, to help you stay abreast of industry trends and expand your knowledge base.

Utilize UWM’s Marketing Tools: UWM provides a comprehensive suite of marketing tools and resources to help you generate leads and attract new clients.

Build Relationships with Your UWM Account Manager: Your dedicated UWM account manager is a valuable asset. They can provide personalized support, answer your questions, and help you navigate complex situations.

How to Get a UWM Mortgage

You can’t apply for a mortgage directly through UWM. You must work with an independent mortgage broker who partners with them. Here’s the process:

Find a Mortgage Broker: Research and select a reputable independent mortgage broker in your area.

Consultation: Discuss your financial situation and mortgage needs with your broker.

Loan Application: Your broker will submit your loan application to UWM (or other lenders, depending on your needs).

Underwriting and Approval: UWM will underwrite and process your loan.

Closing: If approved, you’ll close on your mortgage with your broker.

UWM’s Loan Products

UWM offers a comprehensive suite of mortgage products, including:

Conventional Loans: Fixed-rate and adjustable-rate mortgages for borrowers with good credit. FHA Loans: Government-backed loans with lower down payment requirements, suitable for first-time homebuyers. VA Loans: Loans for eligible veterans and active-duty service members, often with no down payment. USDA Loans: Loans for rural homebuyers, offered by the U.S. Department of Agriculture. Jumbo Loans: Loans for high-value properties that exceed conventional loan limits. Renovation Loans: Loans that allow borrowers to purchase and renovate a property.

FAQs about United Wholesale Mortgage

Is UWM a lender or a broker?

UWM is a wholesale mortgage lender, not a broker. They partner with independent mortgage brokers who work directly with borrowers.

What types of loans does UWM offer?

UWM offers a variety of conventional, government-backed, and jumbo loan options.

How do I apply for a mortgage through UWM?

You cannot apply for a mortgage directly through UWM. You will need to contact an independent mortgage broker who partners with UWM.

Is UWM a reputable company?

UWM is a publicly traded company (NYSE: UWMC) and is a leader in the wholesale mortgage industry.

Conclusion

United Wholesale Mortgage is a leading provider of wholesale mortgage solutions for independent mortgage brokers. UWM’s wide range of loan products, competitive rates, and commitment to technology make it a valuable partner for brokers who are looking to originate loans quickly and efficiently.

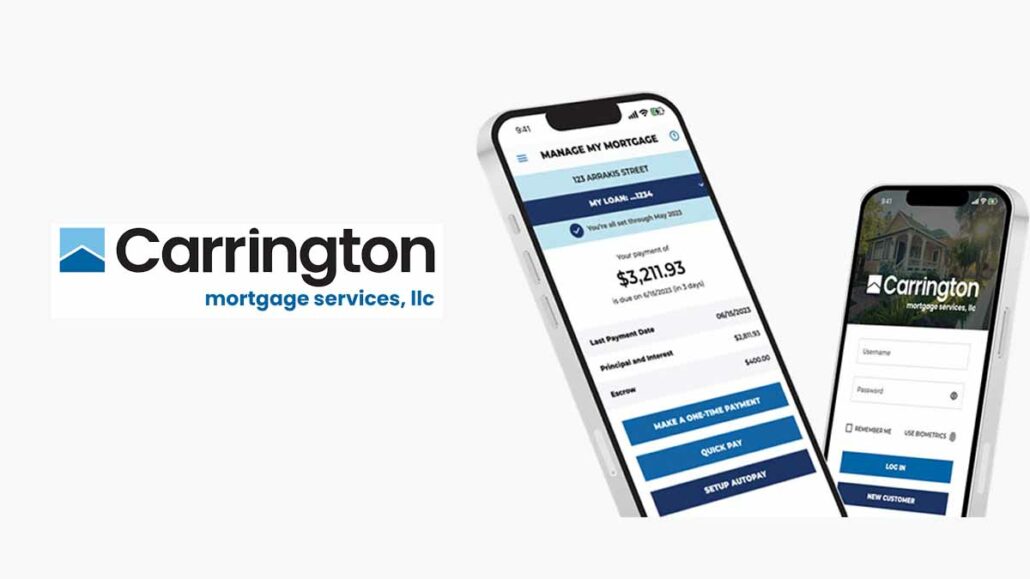

Are you ready to unlock the door to your dream home? Carrington Mortgage can be your trusted partner throughout the mortgage process. This in-depth guide will equip you with everything you need to know about Carrington Mortgage, from their competitive rates and loan options to insightful reviews and valuable resources.

Carrington Mortgage is a leading mortgage lender and servicer in the United States, offering a wide range of loan options for home purchases, refinances, and equity access. Whether you’re a first-time homebuyer, looking to refinance your existing mortgage, or seeking to tap into your home’s equity, it can help you achieve your financial goals.

Who is Carrington Mortgage?

Established in 2006, Carrington Mortgage has become a prominent player in the mortgage industry. They offer a wide range of loan products catering to various borrower needs, including:

Purchase Loans: Fulfill your dream of homeownership with Carrington’s purchase loan options, including conventional, FHA, VA, and USDA loans.

Refinance Loans: Lower your monthly payment, access home equity, or consolidate debt with Carrington’s diverse refinance programs.

Down Payment Assistance: it offers various down payment assistance programs to help first-time homebuyers bridge the gap toward their dream home.

Why Choose Carrington Mortgage?

Several factors set carrington apart from the competition:

Extensive Loan Portfolio: Carrington boasts a comprehensive loan portfolio catering to diverse borrower profiles, credit situations, and down payment capabilities.

Competitive Rates: Carrington is committed to offering competitive mortgage rates, ensuring you get the best possible deal on your loan.

Streamlined Process: Carrington’s online platform and experienced loan officers facilitate a smooth and efficient mortgage application process.

Exceptional Customer Service: Carrington prioritizes customer satisfaction, providing dedicated support throughout the loan journey.

Services Offered by Carrington Mortgage

Home Purchase Loans: Carrington provides various loan options for homebuyers, including government-backed and conventional loans, catering to first-time buyers and seasoned homeowners alike.

Mortgage Refinancing: The company offers refinancing options to help homeowners lower their interest rates, reduce monthly payments, or access home equity.

Real Estate Agent Services: Through its network, Carrington connects clients with experienced real estate agents to facilitate smooth property transactions.

Insurance Services: Carrington also provides insurance services, ensuring clients have access to comprehensive coverage options for their homes.

Loan Programs Available

It offers a variety of loan options to fit your specific needs. Here’s a closer look at some popular choices:

Conventional Loans: These loans are not insured by the government and typically require a minimum credit score and down payment.

FHA Loans: Backed by the Federal Housing Administration, FHA loans offer lower credit score requirements and flexible down payment options.

VA Loans: Veterans and eligible service members can access VA loans with favorable terms, including no down payment in many cases.

USDA Loans: USDA loans are designed for rural homeownership, offering low or no down payment options for eligible borrowers in designated areas.

Understanding Non-QM Loans

Definition and Purpose: Non-QM loans are designed for borrowers who don’t fit the conventional lending criteria, providing alternative pathways to homeownership.

Eligibility Criteria: Eligibility for Non-QM loans varies but often includes considerations of alternative income documentation, higher debt-to-income ratios, or recent credit events.

Benefits and Risks: Benefits of Non-QM loans include flexible qualification requirements and personalized loan terms. However, they may come with higher interest rates and stricter repayment terms, reflecting the increased risk to lenders.

Carrington Mortgage Rates

However, Carrington Mortgage offers competitive rates, but the specific rate you qualify for will depend on various factors, including:

Loan Type: Interest rates differ between loan types (purchase vs. refinance) and government-backed programs (FHA, VA, USDA) vs. conventional loans.

Credit Score: A higher credit score typically translates to a lower interest rate.

Loan-to-Value Ratio (LTV): The ratio of your loan amount to the property value can influence your interest rate.

Down Payment: A larger down payment often leads to a more favorable interest rate.

Reviews

Customer reviews offer valuable insights into Carrington Mortgage’s services. While experiences may vary, Carrington generally receives positive feedback for:

Knowledgeable and helpful loan officers

Streamlined online application process

Competitive mortgage rates

Commitment to customer satisfaction

Is Carrington Mortgage Right for You?

Carrington Mortgage is a strong contender for borrowers seeking a reliable lender with a diverse loan portfolio, competitive rates, and a focus on customer service. To determine if Carrington Mortgage is the right fit for you, consider these factors:

Your Loan Needs: Do they offer the specific loan type you require?

Your Credit Score: Do their credit score requirements align with your profile?

Your Down Payment: Do they offer down payment assistance programs if needed?

Taking the Next Step

Ready to explore your mortgage options with Carrington Mortgage? Here’s how to get started:

Visit their website: Carrington Mortgage’s website provides a wealth of information, including loan options, eligibility requirements, and online application tools.

Contact a Loan Officer: Carrington’s experienced loan officers can answer your questions and

By leveraging this comprehensive guide, you’re well-equipped to make informed decisions about your Carrington Mortgage journey. Take charge of your finances.

Conquering the Mortgage Process with Carrington

Here are some valuable tips to ensure a smooth experience with Carrington Mortgage:

Gather necessary documents: Prepare proof of income, employment verification, tax returns, and bank statements for a streamlined application process.

Understand your credit score: Knowing your credit score empowers you to negotiate better rates. Aim to improve your credit score before applying if possible.

Shop around and compare rates: Don’t settle for the first offer. Compare rates from multiple lenders to secure the best deal.

Communicate effectively: Maintain clear communication with your loan officer throughout the process. Don’t hesitate to ask questions or seek clarification.

Comparing Carrington Mortgage to Competitors

Carrington Mortgage Services (CMS) competes with several well-known mortgage lenders in the industry. When evaluating CMS against competitors like Rocket Mortgage, Wells Fargo, and Freedom Mortgage, it’s essential to compare factors such as interest rates, loan options, customer service, and overall borrower experience.

Interest Rates & Fees:Carrington Mortgage offers competitive interest rates, but they can be higher than some mainstream lenders due to its focus on borrowers with lower credit scores and Non-QM loans.

Loan Options: Carrington Mortgage specializes in government-backed and Non-QM loans, whereas some competitors focus primarily on conventional loans.

Credit Score Requirements: Carrington Mortgage caters to borrowers with lower credit scores, making it a viable option for those who might not qualify with other lenders.

Customer Service & Reviews: Customer experience varies significantly among mortgage lenders. Carrington Mortgage receives mixed reviews, with some praising its flexible loan options while others cite issues with loan servicing.

Loan Servicing & Payment Options: Many borrowers continue to work with their lender after closing for loan servicing. Carrington Mortgage has received some complaints regarding its loan servicing.

FAQs

What are the benefits of using Carrington Mortgage?

Carrington Mortgage offers a variety of benefits, including a wide range of loan options, a streamlined process, and exceptional customer service.

What loan programs does Carrington Mortgage offer?

Carrington Mortgage offers a variety of government-backed and conventional loan programs, including FHA loans, VA loans, USDA loans, and conventional fixed-rate and adjustable-rate mortgages (ARMs). They also offer home equity loans and lines of credit.

How do I get started with Carrington?

You can visit Carrington Mortgage’s website (https://www.carringtonmortgage.com/) to learn more about their loan options and get pre-qualified for a mortgage. You can also contact them directly by phone.

Does Carrington Mortgage offer a mobile app?

Yes, Carrington Mortgage offers a mobile app called Carrington Mobile. With the app, you can manage your mortgage account, make payments, view statements, and more. The app is available for download on the App Store and Google Play.

Carrington Mortgage is a reputable lender with a strong track record of helping borrowers achieve their homeownership goals. By considering Carrington Mortgage for your mortgage needs, you can ensure a smooth and successful home-buying or refinancing experience.

A 401k is a retirement savings plan offered by employers in the United States. It allows employees to contribute a portion of their pre-tax salary to the plan, which is then invested in various financial instruments, such as stocks, bonds, and mutual funds. The primary goal of a 401k is to help individuals save for their retirement and build a substantial nest egg over time. In this article, we will delve into the details of what a 401k entails, how it operates, and its significance in securing your financial future.

What is a 401k?

A 401k is a tax-advantaged retirement savings plan established by the U.S. government under Section 401(k) of the Internal Revenue Code. It allows eligible employees to contribute a portion of their earnings into the plan, and these contributions are not subject to income tax until withdrawn during retirement. The contributions are often made through automatic payroll deductions, making it convenient for employees to save for their future.

The Benefits of Having a 401k

Tax Advantages: One of the major advantages of a 401k is its tax-deferred nature. The contributions you make to the plan are deducted from your taxable income, reducing your current tax burden. Additionally, the earnings on your investments grow tax-free until you start withdrawing them during retirement when you may be in a lower tax bracket.

Employer Match

Many employers offer a 401k matching program, where they contribute a percentage of the employee’s salary to the plan. This is essentially “free money” for the employee, encouraging them to save more for retirement.

Investment Options

401k plans typically offer a variety of investment options, ranging from conservative to aggressive. This allows employees to tailor their investments based on their risk tolerance and financial goals.

Portability

If you change jobs, you can often roll over your 401k into your new employer’s plan or an Individual Retirement Account (IRA) without incurring any tax penalties.

How Does a 401k Work?

Employee Contributions: As an employee, you can choose to contribute a portion of your salary to your 401k plan, up to the annual contribution limit set by the IRS. For 2023, the contribution limit is $20,500 for individuals under 50 and $27,000 for individuals aged 50 and above.

Employer Contributions

If your employer offers a matching program, they will contribute a certain percentage of your salary to your 401k, based on the amount you contribute. This employer match varies among companies, but common matching formulas include dollar-for-dollar matching up to a certain percentage of the employee’s salary.

Vesting Period

Employer contributions may be subject to a vesting period, during which you must remain employed with the company for a specific duration to fully own those contributions. Vesting schedules differ among employers, and it’s essential to understand your company’s policy.

Investment Options

Once your contributions are deposited into the 401k account, you can choose how to invest them. Most plans offer a selection of mutual funds, index funds, bonds, and company stock. It’s essential to diversify your investments to reduce risk.

Tax Implications

Contributions made to a traditional 401k are tax-deferred, meaning they are not taxed until you withdraw them during retirement. However, if you opt for a Roth 401k, your contributions are made with after-tax dollars, but your withdrawals during retirement are tax-free.

Withdrawals and Penalties

Withdrawals from a 401k are generally allowed after reaching the age of 59 ½ without incurring any penalties. However, if you withdraw funds before this age, you may be subject to an early withdrawal penalty of 10% in addition to income taxes.

Types of 401(k) Plans

Traditional 401(k)

How It Works: Contributions are made pre-tax, reducing your taxable income for the year.

Taxes: Withdrawals in retirement are taxed as ordinary income.

Employer Matching: Often available.

Best For: Employees who expect to be in a lower tax bracket in retirement.

2. Roth 401(k)

How It Works: Contributions are made after-tax, meaning you pay taxes upfront.

Taxes: Withdrawals (including earnings) are tax-free in retirement (if the account is held for at least 5 years and the participant is 59½ or older).

Employer Matching: If offered, the employer’s contributions go into a Traditional 401(k) account (taxed upon withdrawal).

Best For: People who believe their tax rate will be higher in retirement or want tax-free withdrawals.

3. Safe Harbor 401(k)

How It Works: Similar to a Traditional 401(k), but employers must make mandatory contributions to employees’ accounts.

Employer Matching: Required by law. Employers must either:

Match 100% of contributions up to 3% of salary and 50% of the next 2%

OR contribute 3% of an employee’s salary for all eligible employees, regardless of participation.

Best For: Employers who want to avoid certain IRS compliance tests while offering strong benefits.

4. SIMPLE 401(k) (Savings Incentive Match Plan for Employees)

How It Works: Designed for small businesses (with 100 or fewer employees).

Employer Matching: Required; employers must either:

Match 100% of contributions up to 3% of salary

OR contribute 2% of salary for all eligible employees (whether they contribute or not).

Best For: Small business owners looking for a low-maintenance retirement plan.

5. Solo 401(k) (Individual 401(k))

How It Works: For self-employed individuals and business owners with no employees (except a spouse).

Contribution Limits: You can contribute as both:

Employee: Up to $23,000 (2024 limit, or $30,500 if 50+).

Employer: Up to 25% of business income, with a total cap of $69,000 ($76,500 if 50+).

Best For: Freelancers, self-employed individuals, or small business owners without employees who want high contribution limits.

6. Profit-Sharing 401(k)

How It Works: Employers make discretionary contributions based on company profits.

Employee Contributions: Can be paired with a Traditional or Roth 401(k).

Best For: Businesses that want to reward employees based on company performance.

7. Tiered 401(k)

How It Works: Allows employers to set different contribution match percentages for different groups of employees (e.g., executives vs. regular employees).

Best For: Companies that want to offer higher benefits to top executives while staying compliant with IRS rules.

The Advantages of Starting Early

Starting a 401k as early as possible can provide several significant advantages:

Compound Interest

The power of compounding allows your investments to grow exponentially over time. By starting early, you give your money more time to grow, potentially leading to substantial gains in the long run.

Financial Security

A well-funded 401k can provide financial security during retirement, reducing reliance on government programs and enabling you to maintain a comfortable lifestyle.

Employer Match

Taking advantage of an employer match can significantly boost your retirement savings, setting you up for a more prosperous future.

Retirement Readiness

The earlier you start contributing to a 401k, the more prepared you’ll be for retirement, as you’ll have had more time to build a substantial nest egg.

401(k) Withdrawal Rules & Penalties

1. When Can You Withdraw From a 401(k)?

Age 59½: Withdrawals are penalty-free, but traditional 401(k) withdrawals are taxed.

Required Minimum Distributions (RMDs) at age 73: Traditional 401(k) holders must start withdrawing.

2. Early Withdrawal Penalties

Before age 59½: 10% early withdrawal penalty + income taxes (exceptions apply, such as disability or first-time home purchase).

Maximizing Your 401(k) Potential

Contribute as Much as Possible: Aim to contribute at least enough to receive the full employer match.

Choose Appropriate Investments: Diversify your investments based on your risk tolerance and time horizon. Consider target-date funds for a hands-off approach.

Review Your Investments Regularly: Monitor your portfolio and make adjustments as needed.

Don’t Withdraw Early: Avoid early withdrawals to prevent penalties and maximize your retirement savings.

Understand Plan Fees: Be aware of any fees associated with your 401(k) plan, as they can impact your returns.

Common 401(k) Mistakes to Avoid

Not Enrolling: Missing out on free employer matching and valuable tax benefits.

Withdrawing Early: Incurring penalties and jeopardizing your retirement savings.

Investing Too Conservatively or Aggressively: Choosing investments that don’t align with your risk tolerance and time horizon.

Ignoring Fees: Allowing high fees to eat into your returns.

Failing to Rebalance: Not adjusting your portfolio to maintain your desired asset allocation.

Common FAQs About 401k Plans

Can I Contribute to a 401k and an IRA Simultaneously?

Yes, you can contribute to both a 401k and an Individual Retirement Account (IRA) simultaneously. However, there are annual contribution limits for each, so it’s essential to ensure you stay within those limits.

Can I Withdraw Funds from My 401k Before Retirement?

In most cases, you can withdraw funds from your 401k before retirement, but you may be subject to an early withdrawal penalty of 10% and income taxes. Some exceptions, such as hardship withdrawals, may allow penalty-free early withdrawals in certain situations.

What Happens to My 401k If I Change Jobs?

If you change jobs, you have several options for your 401k. You can leave it with your former employer, roll it over into your new employer’s plan or an IRA, or cash it out (not recommended due to potential tax implications).

Are There Any Limits on Employer Contributions?

While there is no limit on the percentage of salary an employer can contribute, there is a total contribution limit imposed by the IRS. For 2023, this limit is $61,000 for individuals under 50 and $67,500 for individuals aged 50 and above.

Can I Borrow Money from My 401k?

Some of the plans allow for loans, enabling you to borrow money from your account. However, borrowing from your 401k should be approached with caution, as it may impact your retirement savings and future financial security.

What is the Difference Between a Traditional 401k and a Roth 401k?

The primary difference between a traditional 401k and a Roth 401k lies in the tax treatment. Contributions to a traditional 401k are made with pre-tax dollars, while Roth 401k contributions are made with after-tax dollars. Withdrawals from a traditional 401k are taxed during retirement, while Roth 401k withdrawals are tax-free.

Conclusion

In conclusion, a 401k is an essential tool for securing your financial future during retirement. By understanding how it works, taking advantage of employer matches, and starting early, you can build a substantial nest egg that provides financial security and peace of mind in your golden years. Remember to diversify your investments and consult with a financial advisor to ensure you’re making the most of this valuable retirement savings option.

Motorcycle accidents can be devastating, often leading to serious injuries, financial burdens, and emotional distress. When faced with such a situation, finding the best motorcycle accident lawyer is crucial to securing the compensation and justice you deserve. An experienced attorney understands the complexities of motorcycle accident claims, including dealing with insurance companies, proving liability, and fighting for your rights in court if necessary. With the right legal representation, you can focus on recovery while your lawyer handles the legal challenges.

Choosing the best motorcycle accident lawyer means looking for someone with a proven track record of success, extensive experience in personal injury law, and a deep understanding of motorcycle accident cases. A skilled attorney will not only guide you through the legal process but also ensure that you receive maximum compensation for medical bills, lost wages, and pain and suffering. Whether you’re negotiating a settlement or taking your case to trial, having a dedicated lawyer by your side can make all the difference in achieving a favorable outcome.

Why You Need a Specialized Motorcycle Accident Lawyer

Motorcycle accidents differ significantly from car accidents. They often involve:

More Severe Injuries: Riders are far more vulnerable, leading to catastrophic injuries like spinal cord damage, traumatic brain injuries, and fractures.

Unique Accident Dynamics: Factors like road hazards, rider visibility, and vehicle size play crucial roles.

Bias Against Riders: Insurers and juries may hold preconceived notions about motorcyclists, unfairly blaming them for accidents.

Complex Liability Issues: Determining fault can be challenging, requiring in-depth investigation and expert analysis.

A specialized motorcycle accident lawyer understands these nuances and possesses the expertise to:

Investigate the Accident Thoroughly: Gathering evidence, reconstructing the accident scene, and interviewing witnesses.

Negotiate with Insurance Companies: Protecting you from lowball offers and aggressive tactics.

Build a Strong Case: Demonstrating liability and proving the full extent of your damages.

Represent You in Court: Fighting for your rights if a fair settlement cannot be reached.

Qualities of the Best Motorcycle Accident Lawyer

When searching for legal representation, prioritize these essential qualities:

Experience and Specialization: Look for a lawyer with a proven track record of handling motorcycle accident cases. Ask about their case results and experience with similar injuries.

Knowledge of Motorcycle Laws: They should be well-versed in state and local motorcycle laws, including helmet laws, right-of-way regulations, and traffic codes.

Strong Negotiation Skills: They must be adept at negotiating with insurance companies to maximize your compensation.

Litigation Experience: If your case goes to trial, you need a lawyer with courtroom experience and a history of successful verdicts.

Compassion and Communication: They should be empathetic to your situation and keep you informed throughout the process.

Resources and Network: The best lawyers have access to accident reconstruction experts, medical professionals, and other resources to build a strong case.

Contingency Fee Basis: Most reputable motorcycle accident lawyers work on a contingency fee basis, meaning you don’t pay unless they recover compensation for you.

Finding the Right Lawyer

Seek Recommendations: Ask friends, family, and other motorcyclists for referrals. Online reviews and testimonials can also provide valuable insights.

Research Online: Use search engines to find motorcycle accident lawyers in your area. Pay attention to their websites, online reviews, and professional affiliations.

Check Credentials: Verify the lawyer’s license and disciplinary history through your state bar association.

Schedule Consultations: Meet with several lawyers to discuss your case and assess their experience and compatibility.

Ask the Right Questions: During consultations, inquire about their experience, case results, fees, and communication style.

Evaluate Their Communication: A good lawyer will answer your questions clearly and concisely, demonstrating their expertise and commitment.

Trust Your Instincts: Choose a lawyer you feel comfortable with and confident in their ability to represent you.

Common Challenges in Motorcycle Accident Cases

1. Bias Against Motorcyclists

One of the biggest hurdles in motorcycle accident cases is the unfair bias against motorcyclists. Many people, including insurance adjusters, jurors, and even law enforcement officers, perceive motorcyclists as reckless or irresponsible. This prejudice can influence how fault is determined and may result in lower compensation offers.

2. Proving Liability

Establishing fault in a motorcycle accident is often challenging. Since motorcycles are smaller and less visible, other drivers may claim they didn’t see the rider before the collision. Additionally, proving that the other party was negligent requires solid evidence such as witness statements, traffic camera footage, and accident reconstruction reports.

3. Serious Injuries and High Medical Costs

Motorcyclists lack the same level of protection as car occupants, making them more vulnerable to severe injuries like traumatic brain injuries, spinal cord damage, and broken bones. These injuries often lead to high medical bills, long-term rehabilitation, and lost wages. Insurance companies may try to minimize payouts, leaving victims struggling financially.

4. Insurance Company Tactics

Insurance companies aim to protect their profits and often use tactics to devalue or deny motorcycle accident claims. They may argue that the rider was partially or fully at fault, offer low settlements, or delay payments. Without an experienced motorcycle accident lawyer, victims may find it difficult to negotiate fair compensation.

5. Lack of Proper Evidence

Building a strong case requires substantial evidence, such as accident reports, medical records, expert testimony, and photos from the crash scene. If evidence is not collected promptly, proving negligence can become more difficult, reducing the chances of winning the case.

6. Hit-and-Run Accidents

In some cases, the at-fault driver flees the scene, making it harder to recover compensation. Identifying the driver through surveillance footage, eyewitnesses, or forensic analysis can be time-consuming and challenging. Uninsured motorist coverage may help in such cases, but insurance companies may still resist paying claims.

7. State-Specific Motorcycle Laws

Motorcycle laws vary from state to state, including helmet laws, lane-splitting regulations, and comparative negligence rules. These laws can significantly impact a case, especially if the insurance company argues that the motorcyclist was violating traffic laws at the time of the crash.

8. Delayed Legal Action

Many accident victims delay filing a claim, either due to medical recovery or lack of legal knowledge. However, statutes of limitations set strict deadlines for filing lawsuits. Missing these deadlines can result in losing the right to seek compensation altogether.

What Compensation Can You Recover?

A skilled motorcycle accident lawyer can help you recover compensation for:

Medical Expenses: Past and future medical bills, including hospitalization, surgery, rehabilitation, and medication.

Lost Wages: Income lost due to your injuries, including future earning capacity.

Pain and Suffering: Physical pain, emotional distress, and loss of enjoyment of life.

Property Damage: Repair or replacement of your motorcycle and other damaged property.

Punitive Damages: In cases of gross negligence, punitive damages can be awarded.

FAQ’s

How much does it cost to hire a motorcycle accident lawyer?

Most motorcycle accident lawyers work on a contingency fee basis, meaning they only get paid if you win your case. Their fee is typically a percentage of the settlement or jury award.

How long do I have to file a motorcycle accident claim?

The statute of limitations for filing a motorcycle accident claim varies by state. It’s crucial to contact a lawyer as soon as possible to ensure you meet the deadline.

What if the other driver was uninsured or underinsured?

A skilled lawyer can help you explore options for recovering compensation, such as through your own uninsured/underinsured motorist coverage.

What should I do if the insurance company offers me a settlement?

Do not accept any settlement offer without consulting with a motorcycle accident lawyer. The initial offer is often significantly lower than what you deserve.

Can I still recover compensation if I was partially at fault?

In many states, you can still recover compensation even if you were partially at fault. Your lawyer can help determine how comparative negligence laws apply to your case.

What types of damages can I recover after a motorcycle accident?

You can recover compensation for medical expenses, lost wages, pain and suffering, property damage, and other losses.

How do I find the best motorcycle accident lawyer near me?

Search online directories, read reviews, and ask for referrals from friends, family, or other legal professionals. Schedule consultations with several lawyers to find the best fit for your needs.

Conclusion

Securing the services of the best motorcycle accident lawyer is essential to navigate the legal landscape effectively and ensure just compensation. Their expertise not only alleviates the burden on victims but also upholds the principles of justice.

In today’s fast-paced digital world, digital marketing agencies in New York play a crucial role in helping businesses thrive in an increasingly competitive landscape. With the city being a global hub for commerce, innovation, and technology, companies must establish a strong online presence to stand out. Digital marketing agencies provide expert strategies in search engine optimization (SEO), social media management, pay-per-click (PPC) advertising, content marketing, and more, ensuring businesses reach their target audience effectively. Whether a startup or an established enterprise, these agencies craft tailored marketing campaigns that drive engagement, boost brand awareness, and maximize revenue. Find the best digital marketing agencies in New York. Expert SEO, social media, PPC, and web design services to elevate your brand.

New York is home to some of the most renowned and innovative digital marketing agencies, offering cutting-edge solutions for brands across various industries. These agencies leverage data-driven strategies, advanced analytics, and creative storytelling to deliver measurable results. From small businesses looking for localized marketing solutions to multinational corporations needing global outreach, digital marketing agencies in New York provide the expertise and resources to elevate brands to new heights. With the right agency partnership, businesses can harness the power of digital marketing to stay ahead of the curve and achieve long-term success.

Why Invest in a Digital Marketing Agency in New York?

Local Market Expertise: NYC’s diverse demographics and unique market dynamics require a tailored approach. Local agencies possess intimate knowledge of the city’s trends, consumer behavior, and competitive landscape.

Access to Top Talent: New York attracts the brightest minds in the industry. Partnering with a local agency grants you access to a pool of skilled professionals in SEO, social media marketing, content creation, and more.

Networking Opportunities: NYC is a networking powerhouse. Local agencies often have established connections with media outlets, influencers, and other key players, opening doors to valuable partnerships.

Staying Ahead of the Curve: The digital marketing landscape is constantly evolving. NYC agencies are at the forefront of innovation, ensuring your strategies are cutting-edge and effective.

Top Digital Marketing Agencies in New York

New York is home to numerous esteemed digital marketing agencies. Here, we spotlight some of the leading firms that have made significant contributions to the industry.

MRM

MRM, originally known as McCann Relationship Marketing, is a global direct and digital marketing agency headquartered in New York City. Founded in 1962, MRM has evolved over the decades, merging with various entities and rebranding multiple times to adapt to the changing marketing landscape. Today, it operates under the umbrella of McCann Worldgroup, a subsidiary of the Interpublic Group of Companies.

Core Services Offered

Digital Strategy and Analytics: Crafting data-driven strategies to optimize digital presence.

Content Creation: Developing engaging content across various platforms.

Technology Integration: Implementing technological solutions to enhance marketing efforts.

Customer Relationship Management (CRM): Building and maintaining strong customer relationships through targeted campaigns.

Notable Clients and Projects

MRM has collaborated with several high-profile clients, including:

General Motors: Managing and marketing their digital platforms.

MasterCard: Developing the “Priceless” campaign.

U.S. Army: Creating and maintaining GoArmy.com.

Microsoft: Launching various digital initiatives.

Sullivan & Company

Sullivan & Company, established in 1990 by Barbara Apple Sullivan, is an independent brand engagement firm based in New York City. The agency has carved a niche for itself by focusing on technology, financial services, higher education, and lifestyle sectors.

Digital Marketing: Enhancing online presence through targeted campaigns.

Design and Creative Services: Crafting visually appealing and effective designs.

Content Development: Producing relevant and engaging content.

Notable Clients and Projects

Sullivan has collaborated with several prestigious clients, including:

American Express: Enhancing brand engagement strategies.

Bank of America/Merrill Lynch: Developing integrated marketing campaigns.

LinkedIn: Creating user engagement initiatives.

WebMD: Implementing digital marketing strategies.

R/GA

Founded in 1977, R/GA is a renowned digital design and advertising agency headquartered in New York City. Over the years, R/GA has transformed from a visual-effects company into a full-service agency, offering innovative solutions to global brands.

Consulting and Transformation: Guiding brands through digital transformation.

Notable Clients and Projects

R/GA’s impressive clientele includes:

Nike: Developing the groundbreaking Nike+ platform.

Beats by Dre: Creating impactful advertising campaigns.

Samsung: Designing innovative digital experiences.

Google: Collaborating on various product initiatives.

Services Offered by Digital Marketing Agencies in NYC

Search Engine Optimization (SEO): Boosting your website’s visibility in search results to drive organic traffic.

Pay-Per-Click (PPC) Advertising: Running targeted ad campaigns on platforms like Google Ads and social media to generate leads and sales.

Social Media Marketing (SMM): Building brand awareness, engaging with audiences, and driving conversions through social media platforms.

Content Marketing: Creating valuable and engaging content (blog posts, videos, infographics) to attract and retain customers.

Email Marketing: Nurturing leads and building customer loyalty through targeted email campaigns.

Website Design and Development: Creating user-friendly and visually appealing websites that convert visitors into customers.

Reputation Management: Monitoring and managing your online reputation to build trust and credibility.

Analytics and Reporting: Tracking key performance indicators (KPIs) and providing data-driven insights to optimize your campaigns.

Factors to Consider When Choosing a Digital Marketing Agency

Industry Expertise: Does the agency have experience working with businesses in your industry?

Portfolio and Case Studies: Review their past work to assess their capabilities and results.

Client Testimonials and Reviews: Gauge client satisfaction and agency reputation.

Team and Expertise: Ensure the agency has a team of experienced and skilled professionals.

Communication and Transparency: Look for an agency that prioritizes clear and consistent communication.

Data-Driven Approach: Verify their ability to track and analyze campaign performance.

Pricing and Budget: Consider your budget and ensure the agency’s pricing aligns with your needs.

Agency Culture and Values: Choose an agency that aligns with your company’s culture and values.

SEO Skill: A New York agency must have a strong SEO department. As the city is so competitive, organic ranking is very important.

Local Knowledge: An agency based in New York will have a deeper understanding of the local market and consumer behavior.

How to Choose the Right Digital Marketing Agency in NYC

Define Your Goals: Clearly outline your marketing objectives and desired outcomes.

Research and Shortlist: Conduct thorough research online, read reviews, and ask for referrals.

Evaluate Expertise and Experience: Look for agencies with proven track records in your industry and specific areas of expertise.

Assess Their Portfolio and Case Studies: Review their past work to gauge their capabilities and creative approach.

Consider Their Communication and Collaboration Style: Choose an agency that prioritizes clear communication and fosters a collaborative partnership.

Request Proposals and Compare Pricing: Obtain detailed proposals and compare pricing structures to ensure they align with your budget.

Check for Industry Certifications and Awards: Look for agencies with recognized certifications and industry accolades.

Meet the Team: If possible, meet the team in person to assess their culture and chemistry.

Ask for References: Request references from past clients and contact them to gather insights.

Ensure they understand the NYC market: Ask for examples of local campaigns they have run.

Finding the Best Digital Marketing Agencies in NYC

Utilize search engines with specific keywords like “best SEO agency NYC” or “social media marketing agency New York.”

Explore online directories like Clutch, DesignRush, and UpCity.

Attend industry events and conferences in NYC to network with agencies.

Seek recommendations from business associations and industry peers.

Review agency websites and social media profiles.

FAQ’s

How much does it cost to hire a digital marketing agency in NYC?

Costs vary depending on the agency’s size, expertise, and the scope of services. Expect to pay anywhere from a few thousand dollars per month for basic services to tens of thousands for comprehensive campaigns.

What are the key KPIs to track when working with a digital marketing agency?

Key KPIs include website traffic, lead generation, conversion rates, social media engagement, and return on investment (ROI).

How long does it take to see results from digital marketing campaigns?

Results vary depending on the strategies employed and the competitive landscape. SEO can take several months, while PPC campaigns can generate immediate results.

What questions should I ask a potential digital marketing agency?

Ask about their experience in your industry, their approach to strategy development, their reporting and communication processes, and their pricing structure.

Do I need a full-service digital marketing agency, or can I hire specialists for individual services?

The best approach depends on your needs and budget. A full-service agency offers a comprehensive solution, while specialists can provide focused expertise in specific areas.

How can I ensure my digital marketing agency is transparent and accountable?

Establish clear expectations, request regular reports, and schedule regular meetings to review progress and address any concerns.

What is the difference between SEO and SEM?

SEO (Search Engine Optimization) focuses on improving organic search rankings, while SEM (Search Engine Marketing) includes both SEO and paid advertising (PPC).

How important is local SEO for businesses in NYC?

Local SEO is crucial for businesses targeting customers in specific neighborhoods or boroughs of NYC. It helps improve visibility in local search results.

How often should I update my website’s content?

Regularly updating your website with fresh, relevant content is essential for SEO and user engagement. Aim for at least monthly updates.

How can I measure the ROI of my social media marketing campaigns?

Track metrics such as website traffic from social media, lead generation through social media, and engagement rates (likes, shares, comments).

Conclusion

Choosing the right Digital Marketing Agency in New York is a critical investment that can significantly impact your brand’s success. By understanding the NYC digital marketing landscape, considering key factors, and following a strategic approach, you can find a partner that will help you achieve your marketing goals and outrank your competition in the bustling New York market.

Finding the right Accident Lawyer in Los Angeles can make all the difference when dealing with the aftermath of a serious accident. Whether you’ve been injured in a car crash, motorcycle accident, slip and fall, or any other type of personal injury case, having an experienced legal advocate by your side is crucial. Los Angeles is known for its busy streets and highways, increasing the risk of accidents daily. Navigating complex insurance claims, medical bills, and legal proceedings can be overwhelming, but a skilled accident lawyer can help you fight for the compensation you deserve.

A Los Angeles accident lawyer specializes in protecting victims’ rights and ensuring they receive fair settlements for their injuries, lost wages, and emotional distress. With in-depth knowledge of California personal injury laws, these attorneys can negotiate with insurance companies and, if necessary, take cases to court to secure the best possible outcome. Whether you’re facing minor injuries or long-term disabilities, seeking legal guidance early can significantly impact your case. If you or a loved one has been injured due to someone else’s negligence, hiring a trusted accident lawyer in Los Angeles is the first step toward justice and financial recovery.

The Importance of Hiring an Accident Lawyer in Los Angeles

Accidents happen when we least expect them, and in a bustling city like Los Angeles, the risks are even higher. From car crashes on the 405 Freeway to pedestrian accidents on busy sidewalks, injuries caused by negligence can have devastating consequences. When faced with medical bills, lost wages, and emotional distress, having an experienced Accident Lawyer in Los Angeles by your side is essential. These legal professionals specialize in personal injury cases and can help victims secure the compensation they deserve.

A skilled Los Angeles accident lawyer understands the complexities of California’s personal injury laws and knows how to handle insurance companies that often try to minimize payouts. They gather evidence, negotiate settlements, and, if necessary, represent victims in court to fight for maximum compensation. Without legal representation, accident victims may struggle to prove liability or receive a fair settlement, leaving them burdened with financial and emotional stress. Hiring a knowledgeable accident attorney ensures that your rights are protected and that you have the best chance of recovering damages for medical expenses, lost income, pain, and suffering.

Types of Accidents an Accident Lawyer in Los Angeles Can Handle

Car Accidents: From minor fender-benders to catastrophic collisions, car accidents are a common occurrence in Los Angeles.

Motorcycle Accidents: Motorcycle riders are particularly vulnerable to serious injuries in accidents.

Truck Accidents: Accidents involving large commercial trucks often result in severe injuries and complex legal issues.

Slip and Fall Accidents: Property owners have a duty to maintain safe premises. If you’ve been injured due to a hazardous condition, you may have a claim.

Pedestrian Accidents: Pedestrians struck by vehicles can suffer life-altering injuries.

Bicycle Accidents: Cyclists face significant risks on Los Angeles roads.

Workplace Accidents: Workers’ compensation laws provide benefits to employees injured on the job.

Rideshare Accidents: Accidents involving Uber or Lyft vehicles require specialized knowledge of rideshare insurance policies.

Wrongful Death: If a loved one has died due to someone else’s negligence, you may be able to file a wrongful death claim.

Qualities to Look for in a Los Angeles Accident Lawyer

When searching for the right Accident Lawyer in Los Angeles, it’s essential to find someone who has the experience, skills, and dedication to handle your case effectively. Not all attorneys are the same, and the outcome of your case can depend on the lawyer you choose. To ensure you receive the best legal representation, consider these key qualities:

1. Experience in Personal Injury Law

An experienced accident lawyer should have a strong background in handling personal injury cases. Look for an attorney who has successfully represented clients in car accidents, slip and falls, motorcycle crashes, and other injury claims. Their knowledge of California’s personal injury laws and court procedures can make a significant difference in winning your case.

2. Strong Negotiation Skills

Most accident cases are settled out of court, meaning your lawyer must be an excellent negotiator. Insurance companies often try to offer low settlements, but a skilled attorney will fight to maximize your compensation by presenting strong evidence and countering lowball offers.

3. Trial Experience

While many cases settle, some require litigation. A good accident lawyer should have courtroom experience and be ready to take your case to trial if necessary. An attorney with a strong trial record can put pressure on insurance companies to offer a fair settlement.

4. Proven Track Record of Success

Check the lawyer’s past case results and client testimonials. A lawyer with a history of winning substantial settlements and verdicts for accident victims is more likely to handle your case effectively.

5. Clear Communication and Availability

Legal processes can be complex, and you need a lawyer who will keep you informed. Look for someone who communicates, answers your questions, and is available when you need them. A lawyer who is difficult to reach may not be fully invested in your case.

6. No Upfront Fees (Contingency-Based Payment)

Reputable Los Angeles accident lawyers work on a contingency fee basis, meaning you don’t pay unless they win your case. This ensures that your lawyer is motivated to get the best outcome for you and allows you to pursue justice without financial stress.

7. Compassion and Client-Focused Approach

Beyond legal expertise, a good accident lawyer should genuinely care about your well-being. They should take the time to understand your situation, provide support, and ensure that your best interests are at the heart of their legal strategy.

Top Accident Lawyers in Los Angeles

When seeking legal representation after an accident in Los Angeles, it’s crucial to choose a lawyer with a proven track record, extensive experience, and a client-focused approach. Here are some of the top accident lawyers in Los Angeles:

1. The Dominguez Firm

With over 30 years of experience, The Dominguez Firm has secured over $1 billion for accident victims. They handle various personal injury cases, including car accidents, and offer 24/7 availability.

2. Jacoby & Meyers

Established in 1972, Jacoby & Meyers has won over $2 billion for their clients. They specialize in car accidents and offer free consultations with no fees unless they win your case.

3. Daniel Kim Law Offices

Daniel Kim Law Offices boasts a 98% success rate in car accident cases. Clients can speak directly with Mr. Kim, ensuring personalized attention.

4. McGee Lerer & Associates

This husband-and-wife team offers 24/7 free consultations and has a five-star Yelp rating. They handle car accident cases with a focus on client satisfaction.

5. The Accident Guys

With over 300 million won for clients, The Accident Guys operate on a no-fee-unless-they-win basis. They have garnered over 2,100 five-star reviews, reflecting their commitment to excellence.

6. Law Offices of John C. Ye

With over 1,400 five-star Google reviews, this firm specializes in car accident cases and operates on a no-fee-unless-they-win basis.

7. Heidari Law Group

Heidari Law Group has multiple office locations and offers free consultations for car accident cases.

8. Zarabi Law

Zarabi Law provides personalized attention to car accident victims, ensuring clients receive the compensation they deserve.

9. Law Offices of Edward Y. Lee

Specializing in car accident cases, this firm offers free consultations and has been recognized by Super Lawyers.

10. Compass Law Group

Located in Beverly Hills, Compass Law Group comes highly recommended for their attentive and personable approach to car accident cases.

Choosing the Right Accident Lawyer in Los Angeles:

Experience and Expertise: Look for a lawyer with a proven track record of success in handling accident cases in Los Angeles.

Specialization: Ensure the lawyer specializes in personal injury law and has experience with cases similar to yours.

Reputation and Reviews: Read online reviews and seek recommendations from friends or family.

Communication and Accessibility: Choose a lawyer who is responsive, communicative, and accessible.

Contingency Fee Basis: Most accident lawyers work on a contingency fee basis, meaning they only get paid if you win your case.

Free Consultation: Many attorneys offer free consultations, allowing you to discuss your case and determine if they are a good fit.

Steps to Take After an Accident in Los Angeles

Seek Medical Attention: Your health is paramount. Seek immediate medical attention, even if you don’t feel seriously injured.

Report the Accident: Report the accident to the police and obtain a copy of the police report.

Gather Information: Exchange contact and insurance information with all parties involved. Take photos of the accident scene and any damages.

Document Everything: Keep detailed records of your injuries, medical treatments, lost wages, and other expenses.

Do Not Admit Fault: Avoid making statements that could be interpreted as an admission of fault.

Contact an Accident Lawyer: Consult with an experienced accident lawyer in Los Angeles as soon as possible.

Understanding Compensation in Personal Injury Cases

When an accident results in injuries, victims often face medical bills, lost wages, and emotional trauma. Understanding how compensation in personal injury cases works is essential to ensure you receive the financial recovery you deserve. Compensation, also known as damages, is awarded to accident victims to help them recover from their losses. In Los Angeles, personal injury claims can result in different types of compensation depending on the circumstances of the accident and the extent of the injuries.

Types of Compensation in Personal Injury Cases

1. Economic Damages

Economic damages cover financial losses directly resulting from the accident. These include:

Medical Expenses: Compensation for hospital bills, doctor visits, surgeries, medications, rehabilitation, and ongoing treatments.

Lost Wages: If your injuries prevent you from working, you may be entitled to recover lost income.

Loss of Earning Capacity: If your injuries cause long-term disabilities affecting your ability to work, you may receive compensation for future lost earnings.

Property Damage: If your vehicle or personal belongings were damaged in the accident, you could receive reimbursement for repairs or replacement.

2. Non-Economic Damages

These damages compensate for the emotional and psychological impact of an accident. They include:

Pain and Suffering: Compensation for the physical pain endured due to injuries.

Emotional Distress: Covers anxiety, depression, PTSD, and other psychological effects resulting from the accident.

Loss of Enjoyment of Life: If injuries prevent you from enjoying activities you previously engaged in, you may receive compensation.

Loss of Consortium: If your injuries negatively impact your relationships with your spouse or family, damages may be awarded.

3. Punitive Damages

Punitive damages are awarded in rare cases where the at-fault party acted with extreme negligence or intentional misconduct. These are meant to punish the responsible party and deter similar behavior in the future. For example, if a driver was under the influence and caused a severe accident, a court may award punitive damages.

Common Challenges in Personal Injury Claims

Filing a personal injury claim may seem straightforward, but many accident victims face obstacles that can delay or reduce their compensation. Insurance companies, legal complexities, and proving liability are just a few of the hurdles that can arise. Understanding these common challenges in personal injury claims can help you prepare for potential difficulties and strengthen your case.

1. Proving Liability and Negligence

To win a personal injury case, you must prove that another party’s negligence caused your injuries. This requires showing:

The at-fault party had a duty of care (e.g., drivers must follow traffic laws).

They breached that duty (e.g., reckless driving or unsafe property conditions).

Their breach directly caused your injuries.

You suffered damages (medical bills, lost wages, etc.).

Insurance companies often argue that the victim shares some blame or that there isn’t enough evidence to prove negligence. Gathering police reports, medical records, witness statements, and video footage can help strengthen your claim.

2. Dealing with Insurance Companies

Insurance companies are not on your side—they are businesses that aim to minimize payouts. Some common tactics they use include:

Delaying Claims: They may take weeks or months to process your case, hoping you’ll settle for less out of frustration.

Offering Lowball Settlements: Initial settlement offers are often much lower than what victims deserve.

Denying Claims: Insurers might argue that your injuries are not severe or pre-existing.

Using Statements Against You: Anything you say to an adjuster can be used to reduce your compensation.

A Los Angeles accident lawyer can handle negotiations and prevent insurance companies from taking advantage of you.

3. California’s Comparative Negligence Law

California follows a comparative negligence system, meaning your compensation can be reduced if you are found partially at fault. For example:

If you are 20% responsible for a car accident, your compensation will be reduced by 20%.

If your damages total $100,000, you would receive $80,000 after the deduction.

Insurance companies may exaggerate your fault to lower their payout. A lawyer can counter these claims with evidence.

4. Proving the Extent of Injuries

Insurance companies may downplay the severity of your injuries, arguing that:

You had a pre-existing condition that caused your pain.

The injuries are not as serious as you claim.

You didn’t seek medical treatment right away, implying the injury wasn’t severe.

To counter this, keep all medical records, follow your doctor’s treatment plan, and document any pain or limitations you experience.

5. Statute of Limitations

In California, you have two years from the date of the accident to file a personal injury lawsuit. If you wait too long, you lose your right to compensation.

Exceptions apply in some cases:

If the injury was not immediately discovered, the clock starts when the injury is diagnosed.

If the defendant is a government entity (e.g., a city bus accident), you may have only six months to file a claim.

A lawyer ensures you meet all deadlines and don’t miss your chance to recover damages.

6. Getting Fair Compensation for Non-Economic Damages

Unlike medical bills and lost wages, pain and suffering or emotional distress don’t have fixed dollar amounts. Insurance companies may downplay emotional distress and refuse to offer fair compensation for:

Chronic pain

Anxiety, PTSD, or depression

Loss of enjoyment of life

An experienced attorney will calculate a fair value for these damages and fight to ensure you receive the full amount.

7. When a Case Goes to Trial

Most personal injury claims settle out of court, but some require litigation. Challenges with trials include:

Longer timelines: Lawsuits can take months or years.

Higher legal costs: Going to court involves more resources and legal fees.

Unpredictable jury decisions: A jury might award less than a settlement offer.

A strong lawyer can determine whether accepting a settlement or going to trial is in your best interest.

The Legal Process for Personal Injury Cases in Los Angeles

Navigating the legal process after a personal injury in Los Angeles can be daunting. Here’s a breakdown of the typical steps involved:

1. Initial Consultation and Case Evaluation

Seeking Legal Counsel: The first step is to consult with a qualified personal injury attorney. They will evaluate your case, explain your rights, and determine if you have a valid claim. During this consultation, you’ll discuss the details of your accident, your injuries, and any related losses.

Case Assessment: The attorney will assess the strength of your case, considering factors like liability, damages, and available evidence.

2. Investigation and Evidence Gathering

Evidence Collection: This phase involves gathering crucial evidence to support your claim, including:

Police reports

Medical records and bills

Witness statements

Photographs and videos of the accident scene

Employment records to document lost wages

Establishing Liability: Your attorney will work to establish that the other party was at fault for your injuries.

3. Demand and Negotiation

Demand Letter: Once the investigation is complete, your attorney will send a demand letter to the at-fault party or their insurance company. This letter outlines your damages and demands compensation.

Negotiations: Negotiations will commence, with your attorney advocating for a fair settlement. Many personal injury cases are resolved through settlement negotiations, avoiding the need for a trial.

4. Filing a Lawsuit (If Necessary):

Statute of Limitations: In California, there’s a statute of limitations for filing personal injury lawsuits. It’s crucial to file within the prescribed timeframe.

Complaint and Discovery: If a settlement cannot be reached, your attorney will file a lawsuit. The “discovery” phase involves exchanging information with the opposing party, including:

Interrogatories (written questions)

Depositions (oral testimony under oath)

Requests for documents

5. Mediation and Trial:

Mediation: Many courts encourage mediation, where a neutral third party helps facilitate settlement negotiations.

Trial: If a settlement is not reached, the case proceeds to trial. At trial, both sides present evidence and arguments to a judge or jury, who will then render a verdict.

FAQ’s

How much does it cost to hire an accident lawyer in Los Angeles?

Most accident lawyers in Los Angeles work on a contingency fee basis, meaning they only get paid if you win your case. The fee is typically a percentage of your settlement or court award.

How long do I have to file an accident claim in California?

The statute of limitations for personal injury claims in California is generally two years from the date of the accident. However, there are exceptions, so it’s essential to consult with an attorney as soon as possible.

What damages can I recover in an accident claim?

You may be able to recover damages for medical expenses, lost wages, pain and suffering, emotional distress, property damage, and other losses.

What if the other party doesn’t have insurance?

If the other party is uninsured or underinsured, your own insurance policy may provide coverage. An accident lawyer can help you navigate these complex situations.

Should I accept the insurance company’s first settlement offer?

It’s generally advisable to consult with an accident lawyer before accepting any settlement offer from an insurance company. The initial offer is often significantly lower than what you may be entitled to.

How long will my accident case take to resolve?

The duration of an accident case varies depending on the complexity of the case, the severity of the injuries, and the willingness of the parties to negotiate. Some cases may settle within months, while others may take years to resolve.

What if I was partially at fault for the accident?

California follows a comparative negligence rule, meaning you may still be able to recover damages even if you were partially at fault. However, your compensation will be reduced by your percentage of fault.

A car accident lawyer in San Antonio is essential for anyone involved in a serious vehicle collision. Car accidents can lead to devastating physical injuries, emotional distress, and financial burdens due to medical bills, lost wages, and vehicle repairs. Navigating the legal system on your own can be overwhelming, especially when dealing with insurance companies that may try to minimize your compensation. A skilled San Antonio car accident attorney understands Texas traffic laws, insurance policies, and the tactics used by insurers, ensuring you get the compensation you deserve.

With a dedicated car accident lawyer in San Antonio, victims can focus on their recovery while their attorney handles negotiations, evidence collection, and legal paperwork. Whether it’s a minor fender-bender or a catastrophic accident, legal representation can make a significant difference in securing a fair settlement or taking the case to court if necessary. By working with an experienced attorney, accident victims can protect their rights and improve their chances of obtaining maximum compensation for their losses.

Why You Need a Car Accident Lawyer in San Antonio

Following a car accident, you may face pressure from insurance companies to settle quickly and for less than you deserve. A seasoned car accident lawyer in San Antonio will:

Protect Your Rights: They understand Texas traffic laws and insurance regulations, ensuring your rights are safeguarded.

Investigate the Accident: They will gather evidence, including police reports, witness statements, and accident reconstruction, to establish liability.

Negotiate with Insurance Companies: They will handle all communication with insurers, advocating for fair compensation for your injuries, lost wages, and property damage.

Calculate Your Damages: They will accurately assess your current and future medical expenses, lost earning capacity, and pain and suffering.

Represent You in Court: If a fair settlement cannot be reached, they will aggressively litigate your case in court.

Provide Emotional Support: They will guide you through the legal process, alleviating stress and allowing you to focus on recovery.

Common Causes of Car Accidents in San Antonio